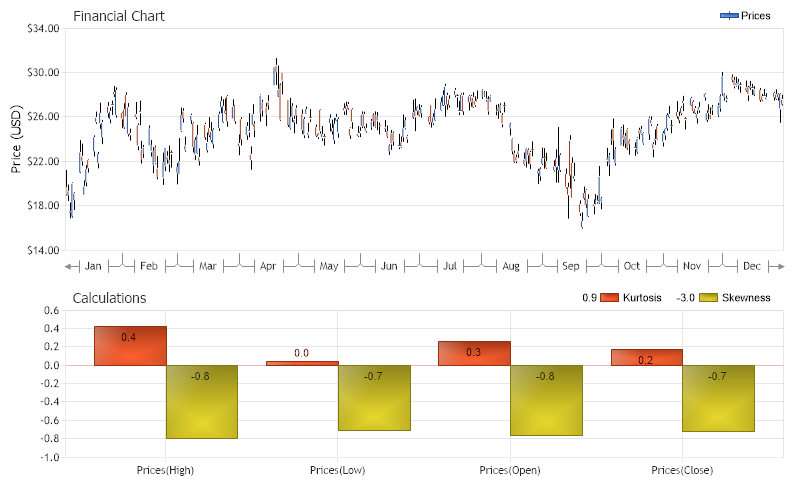

Financial Kurtosis Indicator

Demonstrates the use of one-value financial indicators kurtosis and skewness.

<%@ Page Language="C#" Description="dotnetCHARTING Component" %>

<%@ Register TagPrefix="dotnet" Namespace="dotnetCHARTING" Assembly="dotnetCHARTING"%>

<%@ Import Namespace="System.Drawing" %>

<%@ Import Namespace="System.Drawing.Drawing2D" %>

<%@ Import Namespace="dotnetCHARTING"%>

<html xmlns="http://www.w3.org/1999/xhtml">

<head>

<title>.netCHARTING Sample</title>

<script runat="server">

void Page_Load(Object sender,EventArgs e)

{

// Demonstrates the use of one-value financial indicators kurtosis and skewness.

// The Financial Chart

FinancialChart.Title="Financial Chart";

FinancialChart.TempDirectory="temp";

FinancialChart.Debug=true;

FinancialChart.ShadingEffect = true;

FinancialChart.LegendBox.Template ="%icon %name";

FinancialChart.Size="800X500";

FinancialChart.YAxis.Label.Text = "Price (USD)";

FinancialChart.YAxis.FormatString = "currency";

FinancialChart.YAxis.Scale = Scale.Range;

FinancialChart.TitleBox.Position = TitleBoxPosition.FullWithLegend;

FinancialChart.DefaultTitleBox.Position = TitleBoxPosition.FullWithLegend;

// Modify the x axis labels.

FinancialChart.XAxis.Scale = Scale.Time;

FinancialChart.XAxis.TimeScaleLabels.RangeIntervals.Add(TimeInterval.Month);

FinancialChart.XAxis.TimeScaleLabels.MonthFormatString = "MMM";

FinancialChart.XAxis.TimeScaleLabels.Mode = TimeScaleLabelMode.Hidden;

DataEngine priceDataEngine = new DataEngine ();

priceDataEngine.ChartObject = FinancialChart;

priceDataEngine.ChartType = ChartType.Financial;

priceDataEngine.ConnectionString = ConfigurationManager.AppSettings["DNCConnectionString"];

priceDataEngine.DateGrouping = TimeInterval.Day;

priceDataEngine.StartDate = new DateTime (2021,1,1);

priceDataEngine.EndDate = new DateTime (2021,12,31);

// Here we import financial data sample from the FinancialCompany table from within chartsample.mdb

priceDataEngine.SqlStatement = @"SELECT TransDate, HighPrice, LowPrice, OpenPrice, ClosePrice FROM FinancialCompany WHERE TransDate >= #STARTDATE# AND TransDate <= #ENDDATE# ORDER BY TransDate";

priceDataEngine.DataFields = "xAxis=TransDate,High=HighPrice,Low=LowPrice,Open=OpenPrice,Close=ClosePrice";

SeriesCollection sc = priceDataEngine.GetSeries ();

Series prices = null;

if(sc.Count>0)

prices = sc[0];

else

return;

prices.Type = SeriesTypeFinancial.CandleStick;

CalendarPattern cp = new CalendarPattern (TimeInterval.Day, TimeInterval.Week, "0000001");

prices.Trim (cp, ElementValue.XDateTime);

prices.Name = "Prices";

FinancialChart.SeriesCollection.Add (prices);

FinancialChart.ChartAreaLayout.Mode = ChartAreaLayoutMode.Vertical;

/*

* One-Value Indicators

*/

ChartArea indicatorsChartArea = new ChartArea ("Calculations");

indicatorsChartArea.XAxis = new Axis ();

indicatorsChartArea.YAxis = new Axis ();

indicatorsChartArea.HeightPercentage = 40;

indicatorsChartArea.DefaultElement.ShowValue = true;

FinancialChart.ExtraChartAreas.Add (indicatorsChartArea);

// Kurtosis - calculates the Kurtosis of the currently registered data set.

Series kurtosis = new Series ("Kurtosis");

// If this option is setted true it will allow the user to place all the source values

// into the element�s subValues collection

FinancialEngine.Options.PopulateSubValues = false;

kurtosis.Elements.Add (FinancialEngine.Kurtosis (prices, ElementValue.High));

kurtosis.Elements.Add (FinancialEngine.Kurtosis (prices, ElementValue.Low));

kurtosis.Elements.Add (FinancialEngine.Kurtosis (prices, ElementValue.Open));

kurtosis.Elements.Add (FinancialEngine.Kurtosis (prices, ElementValue.Close));

kurtosis.Type = SeriesType.Bar;

indicatorsChartArea.SeriesCollection.Add (kurtosis);

// Skewness - calculates the skewness of the currently registered data set.

Series skewness = new Series ("Skewness");

skewness.Elements.Add (FinancialEngine.Skewness (prices, ElementValue.High));

skewness.Elements.Add (FinancialEngine.Skewness (prices, ElementValue.Low));

skewness.Elements.Add (FinancialEngine.Skewness (prices, ElementValue.Open));

skewness.Elements.Add (FinancialEngine.Skewness (prices, ElementValue.Close));

skewness.Type = SeriesType.Bar;

indicatorsChartArea.SeriesCollection.Add (skewness);

}

</script>

</head>

<body>

<div style="text-align:center">

<dotnet:Chart id="FinancialChart" runat="server"/>

</div>

</body>

</html>

<%@ Page Language="vb" Description="dotnetCHARTING Component" %>

<%@ Register TagPrefix="dotnet" Namespace="dotnetCHARTING" Assembly="dotnetCHARTING"%>

<%@ Import Namespace="System.Drawing" %>

<%@ Import Namespace="System.Drawing.Drawing2D" %>

<%@ Import Namespace="dotnetCHARTING"%>

<html xmlns="http://www.w3.org/1999/xhtml">

<head>

<title>.netCHARTING Sample</title>

<script runat="server">

Sub Page_Load(ByVal sender As Object, ByVal e As EventArgs)

' Demonstrates the use of one-value financial indicators kurtosis and skewness.

' The Financial Chart

FinancialChart.Title="Financial Chart"

FinancialChart.TempDirectory="temp"

FinancialChart.Debug=True

FinancialChart.ShadingEffect = True

FinancialChart.LegendBox.Template ="%icon %name"

FinancialChart.Size="800X500"

FinancialChart.YAxis.Label.Text = "Price (USD)"

FinancialChart.YAxis.FormatString = "currency"

FinancialChart.YAxis.Scale = Scale.Range

FinancialChart.TitleBox.Position = TitleBoxPosition.FullWithLegend

FinancialChart.DefaultTitleBox.Position = TitleBoxPosition.FullWithLegend

' Modify the x axis labels.

FinancialChart.XAxis.Scale = Scale.Time

FinancialChart.XAxis.TimeScaleLabels.RangeIntervals.Add(TimeInterval.Month)

FinancialChart.XAxis.TimeScaleLabels.MonthFormatString = "MMM"

FinancialChart.XAxis.TimeScaleLabels.Mode = TimeScaleLabelMode.Hidden

Dim priceDataEngine As DataEngine = New DataEngine ()

priceDataEngine.ChartObject = FinancialChart

priceDataEngine.ChartType = ChartType.Financial

priceDataEngine.ConnectionString = ConfigurationManager.AppSettings("DNCConnectionString")

priceDataEngine.DateGrouping = TimeInterval.Day

priceDataEngine.StartDate = New DateTime (2021,1,1)

priceDataEngine.EndDate = New DateTime (2021,12,31)

' Here we import financial data sample from the FinancialCompany table from within chartsample.mdb

priceDataEngine.SqlStatement = "SELECT TransDate, HighPrice, LowPrice, OpenPrice, ClosePrice FROM FinancialCompany WHERE TransDate >= #STARTDATE# AND TransDate <= #ENDDATE# ORDER BY TransDate"

priceDataEngine.DataFields = "xAxis=TransDate,High=HighPrice,Low=LowPrice,Open=OpenPrice,Close=ClosePrice"

Dim sc As SeriesCollection = priceDataEngine.GetSeries ()

Dim prices As Series = Nothing

If sc.Count>0 Then

prices = sc(0)

Else

Return

End If

prices.Type = SeriesTypeFinancial.CandleStick

Dim cp As CalendarPattern = New CalendarPattern (TimeInterval.Day, TimeInterval.Week, "0000001")

prices.Trim (cp, ElementValue.XDateTime)

prices.Name = "Prices"

FinancialChart.SeriesCollection.Add (prices)

FinancialChart.ChartAreaLayout.Mode = ChartAreaLayoutMode.Vertical

'

'* One-Value Indicators

'

Dim indicatorsChartArea As ChartArea = New ChartArea ("Calculations")

indicatorsChartArea.XAxis = New Axis ()

indicatorsChartArea.YAxis = New Axis ()

indicatorsChartArea.HeightPercentage = 40

indicatorsChartArea.DefaultElement.ShowValue = True

FinancialChart.ExtraChartAreas.Add (indicatorsChartArea)

' Kurtosis - calculates the Kurtosis of the currently registered data set.

Dim kurtosis As Series = New Series ("Kurtosis")

' If this option is setted true it will allow the user to place all the source values

' into the element�s subValues collection

FinancialEngine.Options.PopulateSubValues = False

kurtosis.Elements.Add (FinancialEngine.Kurtosis (prices, ElementValue.High))

kurtosis.Elements.Add (FinancialEngine.Kurtosis (prices, ElementValue.Low))

kurtosis.Elements.Add (FinancialEngine.Kurtosis (prices, ElementValue.Open))

kurtosis.Elements.Add (FinancialEngine.Kurtosis (prices, ElementValue.Close))

kurtosis.Type = SeriesType.Bar

indicatorsChartArea.SeriesCollection.Add (kurtosis)

' Skewness - calculates the skewness of the currently registered data set.

Dim skewness As Series = New Series ("Skewness")

skewness.Elements.Add (FinancialEngine.Skewness (prices, ElementValue.High))

skewness.Elements.Add (FinancialEngine.Skewness (prices, ElementValue.Low))

skewness.Elements.Add (FinancialEngine.Skewness (prices, ElementValue.Open))

skewness.Elements.Add (FinancialEngine.Skewness (prices, ElementValue.Close))

skewness.Type = SeriesType.Bar

indicatorsChartArea.SeriesCollection.Add (skewness)

End Sub

</script>

</head>

<body>

<div style="text-align:center">

<dotnet:Chart id="FinancialChart" runat="server"/>

</div>

</body>

</html>